Should JD.com Merge with Vipshop

Chinese e-commerce rivals Alibaba Group Holding (BABA) and JD.com (JD) are taking over the country’s roughly $4 trillion retail market and eclipsing the once-dominant Vipshop (VIPS) .

But while Vipshop’s growth is slowing due to competition from those two, the company still has good fundamentals and would be a smart acquisition for either of them, particularly given the pullback in Vipshop’s shares, KeyBanc Capital Markets CFA Hans Chung wrote in a note to investors on Tuesday. “Financially, we view either deal as possible given significant synergies that could be realized,” he claimed.

Vipshop was founded in 2008 and is the leading online discount retailer in China, best-known for its flash sales. In 2013, Vipshop peaked and earned the title of the highest-valued Chinese e-commerce stock, but it has since fallen behind Alibaba and JD.com.

As of early morning trading on Tuesday, Alibaba’s valuation stood at $424 billion, JD.com’s at $58 billion, and Vipshop’s at $5.3 billion. KeyBanc has “overweight” ratings on the shares of all three companies.

Vipshop’s revenue growth has decelerated from 196% growth in 2012 to 41% growth in 2016. In 2018, KeyBanc estimates the company will see 21% revenue growth. Meanwhile, Alibaba reported 56% revenue growth in 2016 to $33 billion, while JD.com reported 44% revenue growth for 2016 to $37.5 billion.

During the past three years, VIPS has experienced significant multiple compression as investors factor in VIPS’ slowing revenue growth,” Chung noted. However, Vipshop is a valuable takeover target because it still earns the most money per active customer among China’s top e-commerce names (in industry jargon, it has the highest “customer contribution value.”)

While healthy fundamentals, a discounted valuation and a high customer contribution value make Vipshop attractive for both Alibaba and JD.com, an acquisition makes more strategic sense for JD.com because it could strengthen its apparel offerings and boost its female customer base, Chung said. Vipshop gets over half of its revenue from general apparel sales, a category that isn’t a strong suit for the electronics-heavy JD.com. In addition, the majority of VIPS users are female, while the majority of JD.com users are male.

JD could have more upside than BABA,” he explained. Assuming a deal price of $13 (a 44% premium to Vipshop’s current $9 share price), a JD-VIPS combo could have an estimated 55% to 57% upside to the share price in the long term vs. a 10% to 11% upside to the current share price for a BABA-VIPS combo, he said. As of now, only 22% of VIPS active users are also JD.com active users.

Dominant (and much larger) Chinese online retailer Alibaba may not have as much to gain from Vipshop, but it could still benefit from the potential acquisition. The Vipshop platform would give Alibaba’s merchants a place to sell off-season items so that those products don’t compete with their in-season items sold on Alibaba’s huge Tmall platform. Alibaba’s Taobao user base could also be valuable for Vipshop’s flash sales.

Earnings Season

As we move away from earnings season, earnings releases slow and, with the holiday shortened trading in the U.S. next week, macroeconomic data should be slow as well. The general rule is, you don’t short a dull market, and the light data along with the light participation as the summer comes to an end, tends to create dullness. As such, stocks tend to seasonally trade higher around earnings from here and into the middle of September as shown in the chart below.

One statistically bullish indication to support the seasonality over the next couple of weeks is earnings estimates have started moving higher again. In fact, after now holding above a multi-year high, the threemonth earnings estimate revision ratio is above its highest level since estimates rolled over late in 2011. Companies tend to significantly outperform during the 90 days between earnings releases when estimates are revised higher thus, going into the dull part of the quarter, most stocks have positive data. One reason for the strong earnings estimate revisions has been the strong guidance during earnings season – particularly during the month of August. The chart at the top of the next page shows the percentage of companies that provided guidance above estimates during the month of August over the past 15 years. There are still a couple of days in August, so the numbers might change, but so far the percentage of positive guidance announcements relative to the total number of guidance announcements is the highest it has been since 2009. 2009, you might recall, was the first earnings season following the end of the long 2008/2009 recession. The previous peak for the month of August came in 2003 – right after stocks bottomed following the dot.com bubble. In other words, peaks in guidance have come at the start of bull markets rather than at the end and the high percentage of positive guidance announcements suggest estimates are too low.

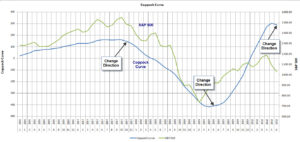

That ties into the chart of the Coppock Curve below too because the August peaks in positive guidance announcements in 2003 and 2009 coincided with the turn higher in the Coppock Curve. The Coppock Curve has been our primary case for being long the stock market since early 2016 and over the past 65 years, bull markets have all lasted until well after the Coppock Curve reached 200. Therefore, we view the positive guidance during the month of August as confirmation that stocks are still trending higher.

If we are going to see a confirmation of continued strength in the stock market, we will likely need to see it in the overall economy too. The chart below shows the net new monthly Non-farm Payrolls as reported by the Bureau of Labor Statistics (BLS) and our Employment Index, which accumulates data from about 50% of the United States and compiles it into one indicator that is concluded roughly a week prior to the BLS’ report. Employment is a lagging indicator, so the stock market, earnings, and the Coppock Curve all typically start moving higher prior to employment data. That was the case in 2009 and, while we didn’t quite see the same downturn in the BLS’s numbers during the earnings recession that ended in the middle of 2016, we did see a downturn in our employment index. Otherwise, the two lines are fairly closely correlated. One exception was the strength shown since the election in our index while the BLS’ numbers have been more muted.

Still, consensus estimates call for the net new jobs during the month of August to fall from the 209,000 jobs added in July to around 165,000 new jobs. Part of this is due to seasonal factors that has skewed the numbers lower over the past several Augusts, but our index also uses seasonally adjusted numbers, and we show employment improved relative to the previous month. Consequently, we see upside potential to the consensus estimates for Friday’s jobs report. That isn’t exactly a bullish indicator for the stock market, but it would give additional confirmation that trends continue higher and that should support the stock market’s seasonality, at least when it comes to trading around earnings, through the holiday and into the middle of September. In the near term, we see a more mixed outlook with our sentiment data continuing to show investors are the most bullish they’ve been in years and our Money Line indicator ticked lower even after the S&P 500 recovered some towards the end of last week. That says, that while the trendline that has now held throughout 2017 continues to hold and the S&P 500 is merely consolidating, there is less money supporting stocks and that favors a break of the trend line rather than a break to the upside. As far as we are concerned, after the S&P 500 pushed above 2,450 and subsequently fell back through, there isn’t much of a reason to be long in the short-term until we are given a buy signal because the risk is for more selling that continues farther than expected. Therefore, while we are trading both long and short around earnings, we will continue to have a short bias while the S&P 500 remains below 2,450.

Leave A Comment