Our featured rolling stock this week is Vipshop (VIPS). We certainly hope that you see the opportunity. Over the last two years Vipshop has given us five (5) opportunities to buy at $10.05. We could have completed a round trip trade a total of three times to buy at $10.05 and sell at $14.90. Each trade (had they been executed) would have resulted in a 48% gain. The overall gain from those three trades would have been a whopping 144%.

Vipshop Holdings Limited is a holding company. The Company is an online discount retailer for brands in China. The Company offers branded products to consumers in China through flash sales mainly on its vip.com Website. The Company’s segment is sales, product distribution and offering of goods on its online platforms. The Company conducts its business through its subsidiaries and consolidated affiliated entities in China. Through its flash sales model, the Company sells limited quantities of discounted branded products online for limited periods of time. The Company offers diversified product offerings from over 17,000 domestic and international brands, including apparel for women, men and children, fashion goods, cosmetics, home goods and other lifestyle products. The Company offers a range of products and services for consumers through lefeng.com, specializing in branded cosmetics, apparel, healthcare products, food and other consumer products.

Earnings Season

We have historically considered earnings season to be the period between Intel’s (INTC) earnings release and Cisco’s (CSCO) earnings release. The world has changed a lot over the years and these two companies are no longer as significant as they have been in the past and they no longer give us the clear bracket to define earnings season, but while there are still companies left to report, by all practical matters, earnings season is now over. Therefore, let’s review what we know. First of all, while these statistics are not really relevant for the overall market since they don’t indicate strength or weakness, there were 485 companies that reported earnings closer to the whisper number than the consensus estimate. Meanwhile, there were 230 earnings releases that were closer to the consensus estimate than they were the whisper. The way we calculate it, the whisper number was more accurate than the consensus estimate 67.8% of the time. This is modestly below our historical average, but still the most reliable published earnings expectation. Just to complete the numbers so far, there were also 70 companies that reported results that differed from both the consensus and the whisper by the same amount and six that were in-line with both.

Our numbers, statistically speaking, are the best indicator of the market’s expectations, but our accuracy isn’t important for the market – rather it is how well the companies reported relative to expectations. Earnings beats for the S&P 500 were rather strong, but when you include companies outside the S&P 500, earnings beats lagged. However, positive guidance announcements, which were already at a multi-year high, have ticked even higher. There are a number of statistically relevant numbers for the overall stock market. One important factor is valuation, which is becoming a concern for the stock market, but our statistics suggest that valuation is only important when considering the direction of earnings estimate revisions. You may recall in past discussions in these pages, or perhaps elsewhere, but ultimately, it is the direction of earnings estimate revisions that separate the left and right hemispheres of the Earnings Expectations Life Cycle. In other words, expensive stocks can continue to move higher as long as estimates move higher, but once estimates begin moving lower, it is the expensive stocks that have farther to fall (of course, there are a number of other factors – primarily investor and analyst sentiment – that determines the top and bottom hemispheres).

Of all the factors that determine whether earnings estimates get revised higher, the single most direct is the company’s guidance. Therefore, the fact that guidance continues to push higher should ultimately push estimates higher too… and we are starting to see just that.

Estimate revisions spiked higher in 2009 to 2011 and, despite a pullback, have remained above where they have been for almost all of the past six years – and are now moving higher again. Statistically speaking, this is a positive for the overall stock market. Now, every time we’ve talked about anything positive of late for the overall stock market we’ve had to qualify that with the risk of the Federal Reserve shrinking its balance sheet… after all, it has made it clear it intends to do so and over the past several decades, the Fed’s liquidity has been the single biggest driver for the stock market. Therefore, it is worth pointing out that over the past week, the Fed added what it sold the previous week. In a perfect world, if you are long the stock market, you want to see the Fed increasing liquidity. That isn’t happening, but we are of the mindset that as long as the Fed isn’t decreasing its assets, the massive amount of liquidity it provided in the past will allow the market to continue to pull the string forward and lift stock prices. Therefore, even though the Fed’s assets didn’t increase to a new high, the fact that the balance is remaining above previous years’ totals is a positive.

That actually fits quite nicely with the historical pattern this time of year – at least when it comes to trading around earnings. The stock market is, as they say, a market of stocks and earnings are the “mother’s milk” for stocks; therefore, as stocks perform around earnings tend to be how the overall stock market performs. The seasonality seldom matches up perfectly throughout the year, but there are almost always periods of correlation throughout the year and, in the past, stocks have bottomed around earnings late in August and continued higher into the early part of September.

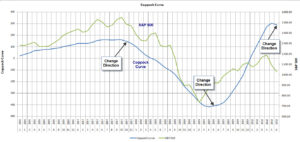

That said, as usual, there is conflicting data. The behavior after companies report earnings isn’t really consistent with the strength in the results and, in many ways, are more consistent with the behavior at a market’s top. Recently we pointed out the reaction after the news was more consistent with the dot.com bubble’s top and that is another warning sign. After earnings, the companies showing the most strength have been the Utilities. That’s important because investor sentiment, at least according to our data is at a high, and inflation has been falling. The chart below shows the normal sector performance during the typical economic cycle and high enthusiasm, peak inflation, and strong sector performance such as the Utilities is what we see late in the cycle and even as a bear market begins. It doesn’t pay to pick tops and we don’t intend to do so, but this is one warning sign worth watching. Despite this warning sign, there is still one other similar data point that is actually positive. While Utilities and Materials may have been the only sectors that have shown strength after reporting earnings, there is another side to the story. Over the past 30 days – – most of that selling has been exactly where it should be: in the stocks in the negative earnings surprise phase of the Earnings Expectations Life Cycle. Investors have been selling those in the negative phase of the life cycle and also those that are value traps – those seeing estimates revised lower. Investors have also been selling the momentum stocks, which may be a sign of the top but is more often just short-term, and those in the positive phase of the life cycle have been getting bought. Quite simply, these are the stocks with a passing whisper score, but they are also those with seeing estimates revised higher while expectations remain low. Coming off a market high, the start of a new cycle in the other direction would generally see selling in all phases of the life cycle and the fact that the positive earnings are still seeing buying is likely not indicative of a market top. That, then, brings us back to the Coppock Curve – our favorite chart since early 2016.

The Coppock Curve is based on the long-term behavior of stock market participants and, over the past 50 years or so, has been the most reliable indicator for the start of an upward cycle in the stock market. The most recent move higher corresponded with the late stages of the earnings recession and, based on past behavior, there is still room for this to play out before the cycle ends. In fact, never once has the stock market topped until well after the Coppock Curve reached 200.

Despite a lack of buying since this past spring, there has also been a lack of selling on the recent weakness. The Money Line – which is a measure of the net buying and selling in the market – has failed to make a lower-low relative to the late June and early July selling. The S&P 500 hasn’t quite made it below the June/July level either, but a sell signal occurs when the Money Line falls below the previous low even as the S&P 500 remains above its previous low. Without the sell signal… and given the other indications, we want to watch for a bounce off the trend line. We’ll likely know when this happens once the S&P 500 gets and holds above 2,450. In the meantime, we must trade what we see rather than what we believe, and that points lower. Consequently, we are trading both long and short around earnings but will favor trading short should the setup present it while the S&P 500 remains below 2,450.

Leave A Comment